.png)

If you’ve been living in Switzerland for a bit, you may have noticed all these advertisements popping up about the 3rd pillar. While it may seem all the rage at the moment, let’s dive deep and figure out what the 3rd pillar is and how you can take advantage of it.

How the Swiss pension scheme works

In Switzerland, the pension scheme (known as the three pillars) is set up as follows: the first and second pillars cover about 60% to 70% of one’s income. The 3rd pillar is intended to close the gap and helps one enjoy the accustomed standard of living after retirement. The third pillar is voluntary and provides for tax-qualified provisions.

For women working part-time, at multiple low-income jobs or not at all, the first and second pillars may hardly cover their pensions at all. According to the Gender Pension Gap study, published in July 2016 by the Federal Social Insurance Office, women’s pensions in Switzerland were 37% less than men, just below the European average. This is the equivalent of CHF20,000 less a year.

The first pillar covers the AHV (old-age, survivors’ and invalidity insurance scheme), the second pillar includes the occupational pension plan and the third includes tax-privileged private savings.

The Swiss Pension Gap

The deficit experienced by Swiss-based women stems largely from the second pillar. The second pillar directly reflects the amount worked and how much was paid in during the working life and penalizes anyone who works part-time or not at all due to care-giving duties or other reasons. In addition, it is impossible to increase one’s work percentage later on in order to fill in the existing gap.

Further, women generally retire earlier and yet live longer and may not be able to rely on their partner’s or spouse’s pension. Even as a working woman, Credit Suisse estimates that a woman would have to set aside about 38% of her income as retirement capital in order to have an adequate retirement provision. Unfortunately, many of us may not achieve this high savings rate consistently over decades.

For married couples, on average, women and men receive a similarly high state pension. This is partly due to splitting: to calculate a pension, the incomes of both members of a married couple are combined, with both partners credited with half each. In addition, child-rearing credits – notional income during the years when children are dependent on care – are granted. Together, that means any gender differences during partners’ periods of unemployment mostly balance out. However, for single women, the picture is different.

An outdated system?

Avenir Suisse makes additional points with respect to the 3rd pillar: today’s gender pension gap reflects the lifestyles of women and men who entered working life in the 1960s and 1970s, and says little about the situation of future female pensioners. Traditional role models were widespread at that time, and far fewer women had conventional jobs than today. This clear division of responsibilities had a particular impact on the gender pension gap in the second pillar.

In recent decades, the pension system has undergone various adjustments to narrow the gender pension gap. One example is the introduction of pension equalization in the second pillar: in case of a divorce, for example, pension entitlements in the pension fund are balanced out between the two partners, primarily benefiting women who were hardly or not at all employed during the marriage (similar to splitting in state pensions). Thus, the pension gap between the sexes will continue to narrow in future even without additional measures.

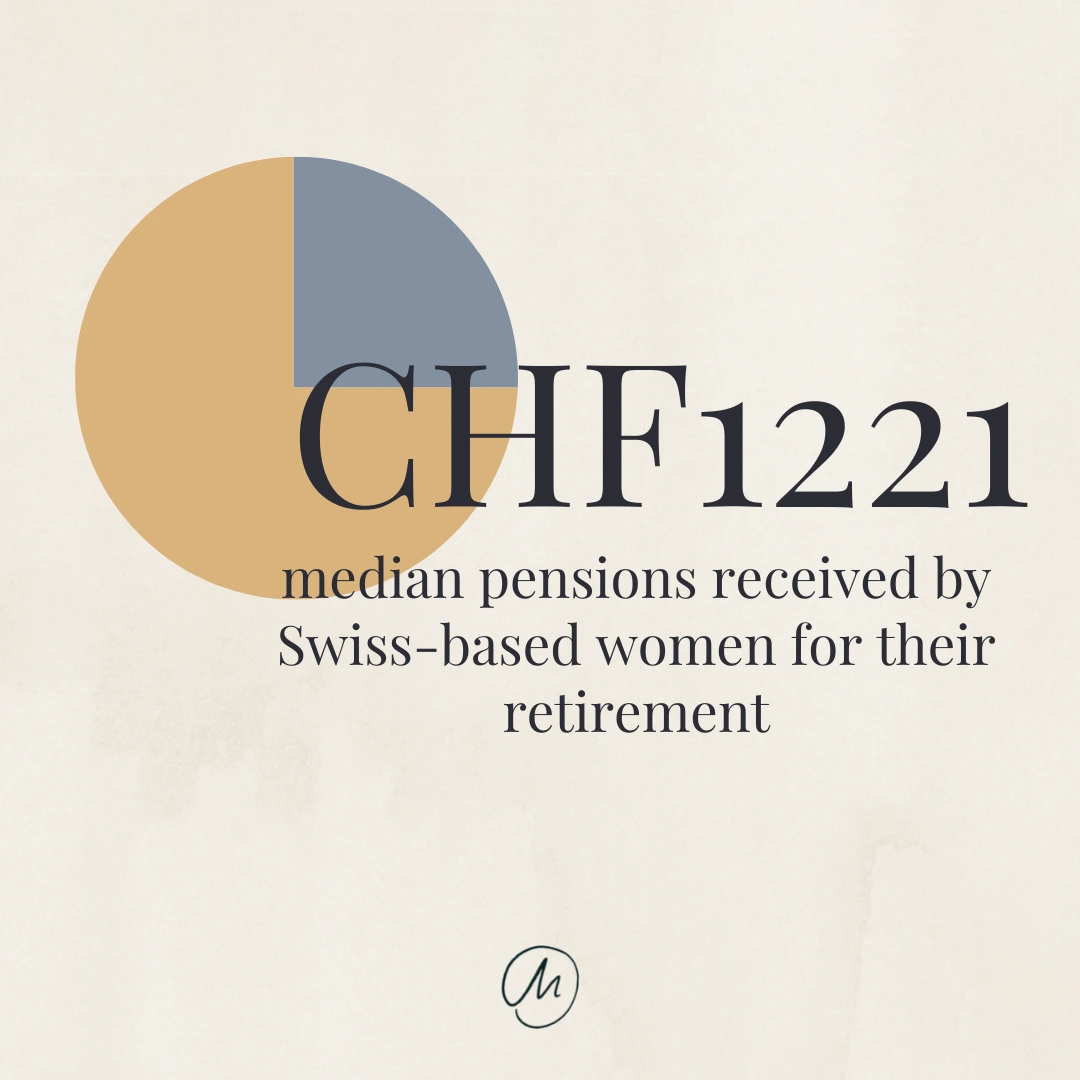

Despite this, in figures from 2017, the most recent available, the median pensions were CHF2301 for men and CHF1221 for women. These women are among the best off among female retirees. The Federal Council also estimates that one third of women do not receive a pension at all. For women, it is clearly not enough to rely on the first and second pillars.

Your chance to counteract the pension gap

This is where the 3rd pillar could help women improve their chances for a solid retirement. Only one in two working women regularly invest in the third pillar, while the corresponding rate for men is almost 60 percent, according to a Credit Suisse study. Opening a 3a pillar with your traditional bank or the more affordable neobanks, is an easy way to get started on saving for one’s future.

CHF1221 – This number is not enough!

Clearly, receiving only CHF1221 a month for a pension would not be enough for most women to maintain their current lifestyles. The average cost of living in Switzerland for a single person is around CHF1467 without rental costs (!), thus this measly sum is hardly enough.

If you’re facing divorce and you happen to earn more than your partner, you may even have to give up a portion of your 2nd pillar to your ex, reducing your potential pension even more.

After my divorce, I put serious thought about my own future. Although I was the primary earner in the relationship, I hadn’t put away enough money for my future. Plus, a good chunk of it was transferred to my ex (as he made considerably less than me at the time). To compensate for this, I started looking into how to maximize my pension planning.

Let’s recap

The 3rd pillar (Pillar 3a) is part of the private pension system in Switzerland. The Swiss pension system is comprised of three pillars:

- 1st pillar – mandatory state benefits (AHV) to cover basic needs following retirement.

- 2nd pillar – mandatory occupational benefits (pension fund or BVG) to provide all employed individuals and intended to provide a ‘comfortable’ income after retirement. Occupational pensions are funded by employer and employee contributions for employed individuals, and voluntarily self-funded by self-employed individuals.

- 3rd pillar (a and b) – private and voluntary provisions intended to maintain the lifestyle you desire post-retirement. These pensions are funded by an individual’s voluntary contributions. This is where you can take advantage of making decisions now that can improve or maintain your future retirement life.

- 3a pillar: Tied pensions. Long-term plans. Capital locked into the retirement plan. Annual contributions are restricted, and the yearly maximums differ depending on whether you have a Pillar 2 occupational benefits plan or not. You can find yearly maximums here.

- 3b pillar: Flexible pensions. Does not have a prescribed or mandatory term and the capital is available at any time. All assets invested or saved voluntarily are counted towards the 3b pillar, including stocks, securities, properties and anything of value such as artworks. Life insurance can also serve as security towards post-retirement.

3a or 3b – What’s the difference?

There are some significant differences between the two 3rd pillars. Below you’ll find a quick overview of these differences.

Restrictions

3a – annual contribution is restricted by Swiss law and whether you have a 2nd pillar which depends on whether you are employed or self-employed. You can find the current yearly maximum here.

3b – no restrictions due to Swiss law apply.

Tax Advantages

3a – Payments are tax-deductible (up to an annual tax advantage of CHF2000) and the money available at retirement is taxed at a special rate (instead of as income).

3b – No tax advantages (although for certain assets, there are no capital gains taxes – check with your tax accountant for further details).

Locking Period

3a – money invested in a 3a pillar is available as early as five years before retirement and under certain circumstances such as buying a house or leaving Switzerland.

3b – money invested in a 3b pillar is available to you at any time.

Alright – what kinds of investments can I make with the third pillar?

Both banks and insurance companies offer 3a pillar pension products.

For 3a, there are:

Interest-bearing 3a account - the interest on your account balance is slightly higher than on a savings account.

- Fixed-interest 3a savings policy - part of the premium is used for risk protection and the remainder earns a fixed rate of interest and is used for retirement savings.

- Unit-linked 3a policy - The savings portion of the premium is invested in funds – the amount paid out at the end of the term depends mainly on the performance of the funds. There are also policies that guarantee a minimum payout when they mature.

- 3a risk insurance - This policy covers the risk of disability and death. It is not a savings policy, so the premiums are comparatively low. However, for myself, I’m not interested in insurance in any case as a way to diversify my investments.

Although funds in a 3a pillar account cannot easily be withdrawn (unless under circumstances) prior to retirement, they do offer certain tax advantages if you pay into them each year.

In addition, the earlier one starts with investing into a 3a account, the more one benefits. However, if you miss the yearly amount to be deposited, you cannot make it up in subsequent years. This is important because not only can you claim the tax benefit only during the year you make a deposit, but also during the entire period until you withdraw, as you do not have to pay any wealth tax on your retirement assets. Since you do not need to declare your retirement assets in your tax return, the income is also tax-free.

For 3b, you can invest in:

- a savings account

- bonds

- equities

- investment funds

- structured products

- insurance policies

Although investments into 3b pillars provide no tax deductions every year like 3a, the biggest advantage is its liquidity. While you cannot deduct the deposits from your taxes and the surrender value is taxed as an asset during the term, at payout the entire amount is tax free, including all earnings and gains.

For example, a savings account is very liquid: you simply go to an ATM or bank branch and withdraw your money. However, do realize that leaving most of your money will expose it to inflation. Inflation slowly eats away at the value of your money, which means your purchasing power declines.

Investing through investment funds and other avenues counteracts this effect of inflation and can even grow your wealth and, thus, set you up for your retirement.

How to withdraw from your 3rd Pillar

Now, you should be aware, though, that you can only withdraw money from a 3a pillar pension plan before reaching retirement age if you want to use it to buy or build a residential property, go abroad to live permanently, or set up your own business.

You can also withdraw your savings if you are unable to work and you draw full invalidity benefit.

You are required to withdraw the accumulated pension capital on retirement (or no earlier than five years before reaching the official retirement age). If you continue to work, it is possible to continue to contribute and/or to postpone the withdrawal for a maximum of five years. Contact your third pillar scheme for the amount of money saved and the terms of withdrawal.

There are no special conditions regarding 3b pillar private pension funds.

If you withdraw funds from a 3rd pillar pension plan before you reach the official retirement age, these will be taxed at a much lower rate and separately from other income. There is a one-off tax which corresponds to the amount that you would pay in one year on this income, however, it is calculated at a reduced rate.

Ah, taxes

When you do withdraw at the time of retirement, be aware that your retirement assets will be subject to taxation. Depending on your cantonal tax residency, your tax burden can be quite high. For example, a withdrawal of CHF100,000 in Herisau AR would make you liable to pay a tax of CHF 7875, whereas in Schwyz, you’d only pay CHF2438.

Due to Switzerland’s complex calculation system, it is difficult to make sweeping generalizations about the level of taxes. One canton may be favorable when it comes to low payout amounts, but be one of the more expensive regions as the payout amounts become larger.

However, you can optimize by doing the following:

- According to finpension.com, setting up a few different 3a pillar accounts may be indeed advantageous. When you draw retirement assets, you pay a reduced tax, which is progressive, similar to the income tax. This implies that the tax is not only higher in Swiss francs and centimes for higher amounts, but also in percentage terms since all lump-sum benefits from the 2nd and 3rd pillar are added together in the same year.

- Pay in before retirement: Because payments into pillar 3a and the pension fund are fully deductible from taxable income during the employment phase, you should take advantage of this as much as possible. You often save more than you will have to pay in taxes when you retire. With each salary increase and in the event of contribution gaps due to training, part-time work or a stay abroad, many employees could make voluntary, tax-attractive purchases into the pension fund.

- Self-employed persons: Doctors, lawyers or entrepreneurs often have some leeway as to what salary they want to insure under the pension plan. From a tax point of view, it can be interesting to settle contributions via the pension fund before retirement, to claim them for income tax purposes and to benefit from the lower tax rate for lump-sum payments after retirement.

- Staggered lump-sum withdrawals: Both Pillar 3a assets and pension fund assets can often be withdrawn in stages. Retirement in several stages is also conceivable - although this is not realistic for everyone. In any case, the tax burden is reduced because the tax progression can be broken by spreading the withdrawals over several years. As a rule, the tax authorities accept a division of pension fund payments into two parts.

- Plan amortization: If you want to reduce the debt on your home, you can draw on your pension assets and use them for amortization. This is best done in several tranches, for example when another tranche of the fixed-rate mortgage falls due. The law allows this only every five years and only for permanently owner-occupied property. This is a much better tax solution than making a large repayment in one fell swoop after retirement.

- Optimization depending on the canton: The taxed amount is often measured according to a certain tax rate. This results in an assumed income that is taxed progressively. Optimization can only be exploited if advice is sought and the system in the respective canton and municipality is taken into account. Of course, it is not forbidden to change your place of residence and, for example, make a vacation spot your main residence. Caution: The new center of life must really be in the new place, and in the case of conspicuously short-term moves, the tax authorities will set certain deadlines.

So, what is the best strategy?

The answer is, it depends. Your situation will be different from mine.

Hence, since I have already paid into a couple of 3a pillar accounts many moons ago, I’ve decided to move these unit-linked policies to another provider in order to save on fees and increase possible returns. In addition, I opted for a unit-linked account/policy originally which invests into stocks instead of an insurance policy to remain somewhat flexible – an insurance policy would not allow me to make staggered withdrawals (nor does it seem to generate much of a return). I have also opened an additional 3a pillar account in order to claim the yearly tax advantage. Read more about 5 top financial investments for higher returns.

Because I’ve learned more about the Swiss 3rd pillar system, I’ve come to realize that my current bank charged way too much for “hosting” my 3a pillars. Although these accounts have made a good return, the fees being charged are still significant. Hence, be sure you know what fees your bank or provider charges you and compare accordingly. If you do find that your bank charges you too many fees, luckily, you can transfer your 3rd pillar to a more reasonably priced provider.

At the moment, for me, I will continue paying the maximum amounts into my 3a pillar accounts, as well as continuing to contribute into my other investment accounts (3b pillars for my case). Although I am aware that my 3a accounts may not grow as fast as my other 3b investment accounts, I am keen on claiming the tax benefits now and during retirement. We have also compiled a list of tips for you on how to become financially independent.

Conclusion

Since I invested in a 3rd pillar scheme some time ago, I knew that after my divorce I needed to take a closer look to see what the Swiss pillar system actually does. Once I did some research on this topic, I was actually quite glad that I had the foresight to invest into the 3rd pillar. Given the pittance of a pension amount given to women at retirement in Switzerland, I felt that this was a step in the right direction. Claiming the tax advantages through multiple accounts, transferring to a cheaper provider while coupling this strategy with using a robo-advisor specialized in 3a accounts will prove a fortuitous move going forward for me.

How about you? Have you contributed to either a 3a or 3b account? To learn more about investing, check out Marmot’s free portfolio check.

++++++

Elsie is a financial writer for Marmot and the woman behind the Swiss-based finance blog Love and Finance. She writes about how to start investing, her own wealth updates as well as about her financial failures (such as never creating a prenuptial agreement). “I've become inspired by others and hope to be an inspiration as well to those who have experienced similar setbacks in love and finance,” explains the 30-something divorcee with a corporate finance background. She never applied what she learned on the job to her personal finance but decided to change that in order to become financially independent -- because there is more to life than just working until retirement.

.webp)

.jpeg)

.svg)